You’ve created a lovely ecommerce store, you’ve filled it with your products and now it’s time to choose a payment gateway so you can accept online payments.

But how do you choose? Who are the best? What fees do they charge? Can they be integrated into your website? Do they accept international payments?

You’ll find below who we believe are the 10 best payment gateways in Ghana you can sign up for to accept online payments and get your ecommerce website running.

Table of Contents

Who are the best payment gateways in Ghana to accept online payments?

Our list of the 10 best payment gateways in Ghana to accept online payments are:

You can read a bit more about each company below and then we’ll cover the various factors that make a payment provider great.

Get your free website audit instantly!

Paystack

Founded in 2015 by Shola Akinlade and Ezra Olubi, Paystack is a Nigerian technology company solving payments problems for ambitious businesses. Their mission is to help businesses in Africa become profitable, envied, and loved.

Trusted by over 60,000 businesses, they launched their services in Ghana in 2020 after an extensive testing phase.

URL: paystack.com

Flutterwave

Founded in 2016 by Iyinoluwa Aboyeji and Olugbenga Agboola, Flutterwave is another payment processor with Nigerian roots but founded in San Francisco, California. They have the largest footprint of any of the companies we studied.

Their vision is to make it easier for Africans to build global businesses that can make and accept any payment, anywhere from across Africa and around the world.

URL: flutterwave.com

theteller

theteller is a payment platform solution brought to you by PaySwitch Ltd., a Ghanaian company established in 2015 by Kojo Choi.

theteller presents an all-in-one payment channel experience where customers can pay from both local and international cards i.e. Mastercard, Visa etc. as well as mobile money services.

URL: theteller.net

DPO

Founded in 2006 by Offer Gat and Eran Feinstein, DPO (Direct Pay Online) started in Kenya but currently has a presence in 23 countries in and outside Africa.

DPO Group currently works with over 100,000 merchants, including 50+ airlines, hotels, restaurants and travel agents all over Africa.

URL: dpogroup.com/online-payments/ghana

iPay

Founded in 2012, iPay is a payments and business management solution that enables businesses and individuals to reach their potential by simplifying their payments, inventory and customer loyalty management.

They have over 5,000 businesses and partners in Ghana that use their platform for receiving payments, managing inventory, paying suppliers, employees and more.

URL: ipaygh.com

- Note: iPay is currently not accepting new signups. They state that this is temporal though so we hope they’ll accept new signups in the near future. Whilst we do not have any insider information, we believe this is connected to their growing partnership with Ecobank.

Slydepay

Slydepay is one of the most popular payment processors according to our 2020 ecommerce in Ghana study and have been been one of the pioneers in the fintech industry.

Founded in 2011 by DreamOval, it was initially called iWallet. They, in partnership with Stanbic Bank, later rebranded and launched the product as Slydepay in 2015.

Stanbic Bank continues to expand the footprint of SlydePay with its introduction in Zimbabwe as well.

URL: slydepay.com.gh

expressPay

Founded in 2012 by Curtis Vanderpuije, expressPay defines itself as an ecommerce marketplace and payment gateway provider. They have one of the most popular payment apps in Ghana.

As a payment gateway provider, they are an official Visa Payment Technology Provider (PTP). Their team has a combined experience of 25+ years in developing software and helping solve key problems for market leaders.

If you pay your taxes online through the Ghana.GOV portal, you may like to know that expressPay is the payment provider.

URL: expresspaygh.com

Hubtel

Hubtel (formerly SMSGH) was founded in 2005 by Alex Bram. A previous payment product they had, MPower Payments, was shut down and launched as a part of Hubtel when they rebranded.

Whilst they provide both SMS and payment solutions, they want to be Africa’s most-loved shopitality platform. They currently have the Hubtel Mall which hosts hundreds of merchants, selling thousands of products.

URL: hubtel.com

Interpay

Interpay is an electronic payment platform that makes transactions and e-commerce simpler, secure, and more convenient. They allow both merchants and consumers to make and receive payments of bills, invoices, and fees.

Founded in 2014 by Saqib Nazir, Interpay was acquired by Emergent Technology (EmTech), a California-based financial technology company in 2018.

myghpay

myghpay is an integrated and secure online payments and collections platform designed to enable individuals, businesses and institutions to make or receive payments online from their homes or offices via the use of a Visa/MasterCard, Gh-link enabled card or mobile wallet.

It was launched by the Guaranty Trust Bank (GT Bank Ghana) in July 2017. They also provide a payment app that allows users to pay for utilities, school fees, insurance and perform other transactions.

URL: myghpay.com

Fees

To enable you accept payments online smoothly, a payment processor has to cover all their expenses and make a profit. They do this by way of fees. There are 6 main types of fees we came across which we’ll be discussing below.

Disclaimer: We do not have all the data we’d like on each of the 10 payment providers discussed. This is mainly because some of them do not publicly display any pricing information. They usually negotiate these directly with their clients.

Thus the information we have below may be subject to change and so do cross-check before signing up with any of them.

Alright, so back to the discussion.

Setup fees

Your payment processor may or may not charge you a setup fee. From what we perceive, this usually has to do with the level of self-service involved in getting you up and running.

Most payment processors that allow you to sign up and be up and running in just a few hours usually do not charge a setup fee.

On the other hand, the payment providers who require extensive documentation and contracts signed usually have a one-time setup fee charged.

expressPay may charge you a setup fee of GHc500 once you’ve completed integrating their payment system into your website and are ready to go live.

Interpay have an onboarding fee of GHc1,000 whilst DPO charges a setup fee of GHc2,400 (or $300) in order to set you up on their platform.

Monthly fees

Our study found that processors charging monthly fees were a bit rare.

Hubtel is the only platform we know of currently who have introduced a GHc25/month fee in order to use their payment platform on your website.

If you choose to sell on Hubtel Mall rather than integrate their payments into your website, then there’s no monthly charge for that.

Percentage transaction fees

The one constant for every single payment processor is the presence of a percentage fee on every transaction. This ensures that they are paid commensurate to the amount of work they do for you, in this case the amount of money they move.

Breaking down the fee structure though is quite complex. This is because they charge their fees differently.

Some charge a single percentage on all transactions with no exceptions (Paystack). Others charge a different percentage based on whether the transaction is local or foreign (Flutterwave, iPay and Interpay).

Some charge a lower percentage on mobile money transactions relative to their other local transactions (DPO) whilst others charge a differing percentage based on the particular mobile money network in question (Hubtel).

There was a range of percentages charged, from a low of 1.9% to a high of 4.5%.

| Payment Processor | Setup Fees | Mobile Money | Local Card | Int. Card |

|---|---|---|---|---|

| Paystack | Free | 1.95% | 1.95% | 1.95% |

| Flutterwave | Free | 2.5% | 2.5% | 3.8% |

| theteller | Free | 2% | 2.5% | 2.5% |

| DPO | GHc1,725 | 3.5% | 4.5% | 4.5% |

| iPay | Free | 1.9%* | 2.5%* | 3.5%* |

| Slydepay | Free | 2% | 3% | – |

| expressPay | GHc500 | 3% | 3% | – |

| Hubtel | GHc300/yr | 1.95% | 1.95% | – |

| Interpay | GHc1,000 | 2% | 2.5% | 3% |

| myghpay | Free | Free | 3% | 3% |

* = iPay charges an additional GHc0.50 for every transaction in addition to the percentage charged.

– = This represents unknown information which we’ll update once we have new information.

With respect to transaction fees, we understand these are a cost of doing business. A payment gateway works hard to ensure they can provide the service they do and the workman is worthy of his wages.

If your payment processor charges a 2% fee and someone pays you GHc100, you end up receiving GHc98 whilst the processor keeps GHc2 as their fee.

One feature a lot of payment gateways have is the ability to choose who pays the required transaction fee. In the scenario above, you the merchant paid that fee.

But you can rather choose to have your customer pay the fee.

When that happens, you receive a full GHc100 for the product you sold and the payment gateway receives their GHc2. In this case, it’s your customer who has to pay an extra GHc2, totaling GHc102.

Whilst we do not recommend this, there may be scenarios where this is the best way to go.

In those scenarios, we advise that you inform your clients or customers well in advance that the final price they pay will be slightly higher than the price displayed.

It is never pleasing to a customer to know they’re paying one amount for a product, only to reach checkout and the amount has increased.

This is why a huge portion of online shoppers abroad abandon their orders.

They get to checkout, see the shipping costs and cancel their order. This has left many retailers with no choice but to offer some manner of free shipping.

An alternative to surprising your customers with extra fees at the checkout point is to price your products in advance with the consideration of any transaction fees you might incur.

Fixed transaction fees

Charging a small fixed fee on every transaction is basically the standard in most developed countries. It was however rare to see that with the payment providers we studied.

Only iPay charged a GHc0.50 fixed fee per transaction. This is in addition to the percentage transaction fee.

Currency exchange fees

When a client pays you with a card in a different currency from what your payment processor or account provides, a currency conversion happens. This is usually done by the client’s bank automatically.

If your payment processor only processes Ghana Cedi transactions, you won’t have to worry about currency exchange fees.

On the other hand, if your payment processor allows you to accept payments in different currencies like Naira, Dollars and Pounds, you should be ready for more fees.

If a client pays you $100 for a product and your processor charges a 2% transaction fee, you will have $98 show up in your account balance with your provider.

To get those $98 into your bank account though may be a slightly different story. This is because your payment provider is now in charge of exchanging those $98 into the Ghana Cedi equivalent and lodging them in your bank account.

When this happens, we can assure you they do not use Google currency convertor or XE.com. The conversion rate they use is solely up to their discretion.

We have signed up for and used almost a dozen payment processors over the years and we are always quite amazed at how much money you can lose through currency conversion.

It certainly depends on the payment processor and the currency in question, but we have seen losses of over 10 to 20% after currency conversion.

If you do plan on receiving a lot of international payments and want to avoid currency conversion losses, you may want to consider a merchant account with a bank.

You’d usually be able to have a Dollar account where your foreign payments would be lodged directly. (Of course you would now be subject to your bank’s currency conversion rates if you choose to withdraw that amount from your account.)

Chargeback fees

The last type of fee we should mention has to do with chargebacks. These fees don’t happen regularly. They only happen in the rare instance that a client of yours tells their bank to reverse a transaction that was made with their card.

For example, someone receives his bank statement and sees he made a payment to your company for a product. He is absolutely certain he didn’t make that purchase and informs his bank of a fraudulent charge on his account that he would like reversed.

Or a customer does make a purchase on your website for an item. He waits for a month and the product never arrives so he lodges a complaint with his bank to retrieve the money that was paid to you. That’s a chargeback.

Banks do not play around with their customers or with fraud. In many cases, they will get that money reversed without any questions asked. To prevent that from happening, you have to make sure you deliver on your promises and keep records of everything!

If you do sadly get hit with a chargeback, your payment processor is not only likely to reverse the amount from your account, but they may also hit you with a penalty or fee for the inconvenience.

Whilst some payment providers do not charge a penalty on chargebacks, most others do not disclose how much a chargeback will cost you. We have seen penalties as high as $35 per chargeback incident.

And if you inconvenience them this way one too many times, they will permanently shutdown your account as being too high-risk.

International Payments

Whilst it’s all nice and good to be able to accept payments from customers in Ghana, a lot of businesses want and need to accept international payments or receive money from customers abroad.

This has been a challenge to the majority of business in Ghana since the dawn of ecommerce in Ghana. Cordelia Salter-Nour, founder of eShopAfrica.com mentions this from almost two decades ago when she was getting her online shop off the ground.

Ghana has been considered a high-risk country when it comes to online transactions. Sadly, a tremendous amount of fraud originates from our country and so most international payment platforms block or ban Ghana outright.

PayPal for example put Ghana on a blacklist which we haven’t gotten off of since. You can’t even find Ghana in the list of countries if you want to make a payment with PayPal.

One of the only international payment providers that used to provide service to Ghana, 2CheckOut, also decided to no longer serve Ghana. This happened right after Avangate acquired 2CheckOut in 2017 (which in turn was acquired by Verifone in 2020).

If you want to accept international payments, you need a payment gateway that not only accepts international payments, but is also willing to have you sign up on their platform.

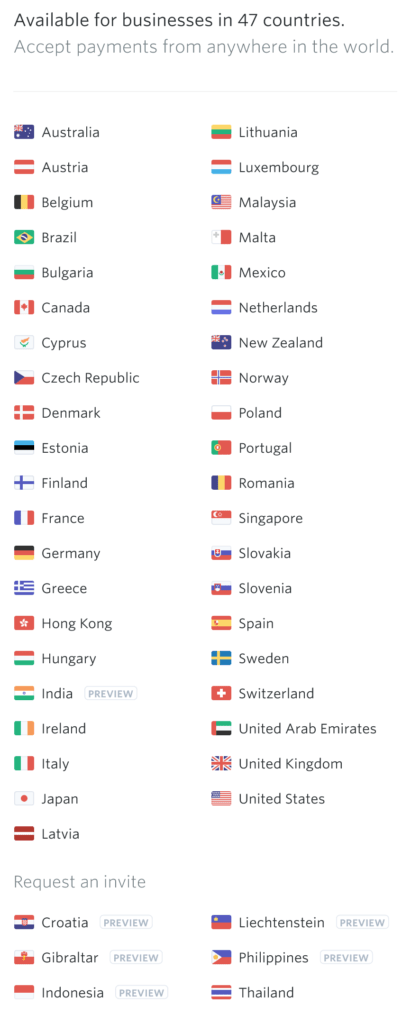

Stripe for example is available to merchants in only 47 countries, none of which are in Africa.

Stripe has recently acquired Paystack though, so who knows, there’s the possibility improved international payment processing capabilities might come to the platform.

Most Ghanaian payment platforms must follow stringent regulations from the Bank of Ghana. This in turn sometimes puts a few stumbling blocks in your path when trying to accept international card payments.

To begin with, many of them are not permitted to charge cards in any other currency other than Ghana Cedis. This makes it awkward for your American customer who knows nothing about Cedis to see her card about to be charged in a different currency.

Another one is verification. Even if your customer goes ahead with the transaction, some processors will instantly demand proof that they are the card holders, be that a scanned copy of the card with their ID or some other form of verification.

Edem Kumodzi, a software architect and program manager at Microsoft, also provided some insight into the issue on Twitter, stating that certain transactions on local payment platforms with foreign or international cards fall into the category of remittances and are thus regulated completely differently.

That being said, majority of the payment processors listed above mention their ability to accept international payments.

We’ve have some success in that arena with Flutterwave and Paystack although we have not had the opportunity to test everyone else on the list.

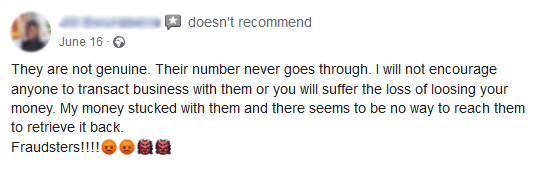

Some users have encountered challenges though. Here is a user complaining about not being able to accept international payments although the gateway he signed up for said he could.

If accepting international payments is an important part of your business, make sure you enquire about any extra requirements needed in order to do so.

Recently, Flutterwave announced a partnership with PayPal enabling Flutterwave merchants in Africa accept international payments from anywhere in the world via PayPal.

This is terrific news and so we decided to test it out to make sure it works as promised. And it did live up to our expectations, initially! Currently though, the feature seems to have been disabled for Ghana. You can read more on that here on how to accept PayPal payments in Ghana.

Multi-currency

Some payment processors which do accept international card payments do so by charging the card in Ghana Cedis as mentioned. This is Ghana’s official currency and what the Bank of Ghana usually allows them to charge cards in.

Other processors though allow you to charge cards in a variety of currencies. DPO states that they “provide businesses with an all-currency, all-payments solution. Your customers can now pay you with their currency of choice”.

Considering the fact that there are 180 active currencies in the world, if DPO is able to charge all these currencies directly, this is quite a feat.

Outside of DPO, Flutterwave comes in next, charging cards in a total of 51 currencies and counting. It’s a long list, but you can scroll through it below:

- UAE Dirham – AED

- Argentine Peso – ARS

- Australian Dollar – AUD

- Bulgarian Lev – BGN

- Brazilian Real – BRL

- Canadian Dollar – CAD

- Swiss Franc – CHF

- Yuan Renminbi – CNY

- Colombian Peso – COP

- Costa Rican Colon – CRC

- Czech Koruna – CZK

- Danish Krone – DKK

- Euro – EUR

- Pound Sterling – GBP

- Ghana Cedi – GHS

- Hong Kong Dollar – HKD

- Hungarian Forint – HUF

- New Israeli Sheqel – ILS

- Indian Rupee – INR

- Japanese Yen – JPY

- Kenyan Shilling – KES

- Moroccan Dirham – MAD

- Macanese Pataca – MOP

- Mauritius Rupee – MUR

- Mexican Peso – MXN

- Malaysian Ringgit – MYR

- Nigerian Naira – NGN

- Norwegian Krone – NOK

- New Zealand Dollar – NZD

- Peruvian Nuevo Sol – PEN

- Philippine Peso – PHP

- Polish Zloty – PLN

- Russian Ruble – RUB

- Rwanda Franc – RWF

- Saudi Riyal – SAR

- Swedish Krona – SEK

- Singapore Dollar – SGD

- Sierra Leonean Leone – SLL

- Thai Baht – THB

- Turkish Lira – TRY

- New Taiwan Dollar – TWD

- Tanzanian Shilling – TZS

- Uganda Shilling – UGX

- US Dollar – USD

- Venuzuelan Bolivar – VEF

- CFA Franc BEAC – XAF

- CFA Franc BCEAO – XOF

- South African Rand – ZAR

- Zambian Kwacha (Pre 2013) – ZMK

- Zambian Kwacha – ZMW

- Zimbabwe Dollar – ZWD

If your business requires charging cards in many different currencies, then your best bets are on DPO and Flutterwave.

Registration Requirements

Signing up for a payment processor is in many cases uneventful. That’s supposed to be a good thing. However different payment processors sometimes require different amounts of data.

When registering as a business, you’re going to need to provide copies of your company’s registration documents and personal identification (although some also require bank statements and more).

A few payment processors allow you to sign up for a personal account or a starter business account. This is a basic account that allows you to accept some transactions and has a low limit regarding the volume of transactions you can accept.

Flutterwave puts a limit on transaction volumes until your account is verified. Paystack has a Starter Business plan that allows businesses that aren’t registered to at least get started with accepting payments online.

iPay has a Basic tier open to individuals, freelancers and unregistered businesses that allow them to accept payments only via mobile money (and QR payments).

To accept card payments through them though, you’ll need to upgrade and provide both business registration documents and a business bank account.

There are some payment processors that take things much further. And this has to do with having a merchant account.

A merchant account is a special bank account that allows a registered business to accept various types of payments including debit and credit card transactions.

Many banks provide the option for you to sign up for a merchant account. Some banks have even provided payment gateways connected to their own merchant accounts.

A few examples include:

Because myghpay is a product of GT Bank (as is GTPay), it requires an account be opened with them. You can see this in section 4 of their registration form.

Due to the account opening and other KYC (Know Your Customer) requirements, it’s a little bit more complex to sign up with myghpay.

If you do choose to have a merchant account for its various advantages, you will most likely have to sign up in person, provide a sufficient amount of documentation and negotiate any transaction fees based on the volume of business you’ll be doing through your merchant account.

Integration, plugins and API libraries

Just as a car is of little use to you if you have no one to drive it, the same way a payment processor might be of little use to you if you can’t actually use it.

Some of the payment gateways allow you to create payment pages or links which you can send to clients and customers to make payment for your products.

However, if you want to get the maximum benefit out of any payment processor, you’re going to need it properly and tightly integrated into your website or application.

We strongly believe that one of the most important factors that determines how well a payment processor is adopted is the availability of a free and available plugin for the most popular website platforms.

This is because the vast majority of business owners who have websites are not programmers or developers. They can manipulate their websites, drag and drop content here and there, and the one thing left is to accept payments.

Plugins make this extremely simple. Simply install the plugin, follow a few instructions and place a few values in some spaces and that’s about it.

When payment processors expect their customers to pay for plugins or hire website designers and developers to integrate a platform into their website by way of their API (Application Programming Interface), we notice a much lower level of patronage of that processor.

Disclaimer: This is sometimes part of a payment processor’s strategy, to ensure they are reaching the customers who they believe are the best fit for them.

Get your free website audit instantly!

So with regards to plugins, we looked at which payment providers had plugins for the major CMSes (Content Management Systems).

We found out that the results mirrored the findings in our study on the platforms and technology used by the ecommerce industry in Ghana.

All of the top 10 payment providers had a plugin for WordPress (WooCommerce to be specific). 7 had one for Magento and 5 for OpenCart.

If your website is developed with the WordPress CMS, they all have you covered. But what if you’re using something slightly less popular, like Prestashop, WHMCS or Drupal?

Then you should probably consider Paystack or Flutterwave. Both had plugins for almost everything. DPO was second with 8 plugins whilst Slydepay had 7.

If you want to accept payments on your custom built website, or in a mobile application rather, you’re going to have to tap into their APIs.

All the payment providers had APIs although not all had publicly accessible documentation. Before you commit to a payment platform, it is useful to be able to read through their documentation to ensure you can work with it.

To make it simpler though, many payment service providers provide libraries or SDKs (Software Development Kits) making it easier for programmers and developers to integrate with their systems.

The most popular programming language library that was available was PHP. Python and .NET were tied in second place. Also in second place were the SDKs for Android and iOS.

As with the plugins issue, so too with the programming languages issue.

If you’re building your app with Node JS, Ruby, Angular or React, which payment providers give you a sufficient amount of direction to make it easy?

Paystack and Flutterwave come out on top again. They provided for all the 11 languages and SDKs mentioned above and even a few extra.

DPO was in second place with 7 whilst expressPay, Hubtel and Slydepay all had 4.

Whilst the stability of the APIs and the quality of a processor’s documentation are also useful things to consider, that’s a little beyond our scope for this article.

We’d love to know your preference and experiences if you develop with any of them.

User Interface

How a gateway presents its payment options, and the ease with which customers can navigate and make payment for orders is very critical to your success as an online business.

You can work very, very hard to get customers to your site, upsell them on your products, only to have them never complete their order because the payment gateway you use was a little too confusing for them.

Two of the main deterrents that will suppress successful checkouts on your site have to do with customers having two many data fields to enter when completing a transaction, and customers having to leave your website.

Whilst it is the standard for most payment processors to take a customer away from the ecommerce website, accept payment details on their own page, and then send the customer back to the website, this is not exactly the simplest process.

Shopify, one of the largest ecommerce platforms in the world, introduced their own payment system in 2013 with one of the main reasons being to improve the payment and checkout experience.

As you can see below, they have seamlessly integrated all the needed payment fields right into the ecommerce site so there is no redirecting the customer away from and back to the site when the order is complete.

The gold standard for simplified checkouts may reside with Stripe though. Not only do they accept payments inline with the checkout process, but they went further to eliminate the name field.

All payment gateways usually redirect customers to their own pages in order to complete orders before redirecting them back. 3 of the companies we studied however do provide an inline checkout experience.

Paystack, Flutterwave and theteller allow your customers to complete their payments without ever leaving your website. They do this via a cute pop-up modal that appears at checkout on your website.

Outside of that, the payment provider will redirect you to their payment page where you’ll be able to select the payment method you prefer to use in completing your order.

How to accept MTN Mobile Money payments online

Because MTN Mobile money is by far the largest mobile money platform in Ghana, with approximately 90% of all mobile money transactions on their network as at 2019, it’s usually the payment method most sought after.

If you’re going to be accepting online payments through your website in Ghana, you’ve definitely got to be accepting MTN Mobile Money.

All the 10 payment platforms we’ve mentioned allow you to process MTN Mobile Money transactions. (To the best of our knowledge, whilst the networks accept all 3 mobile money wallets from telcos, DPO is the only one that processes MTN Mobile Money solely.)

There is something we’ve noticed that you might want to take note of. MTN has gotten a lot of flack when it comes to mobile money fraud and so in a series of moves to clamp down on fraudsters, they’ve also made their network a bit more complex than might be necessary.

The first move about 2 years ago was to disable the automatic prompt that lands on your phone which allows you to complete the transaction. They switched it up in favour of people dialing *170# on their phones to approve of transactions via their My Approvals menu.

They eventually allowed payment processors to display automatic prompts for transactions again but only if the payment gateway verifies the phone number first.

So now most of the payment gateways require you to enter a OTP (One-time password, usually a 4 to 6 digit code) to verify your number if you’ve never paid through their platform before.

Others require you to rather dial a specific shortcode on your phone to complete this verification. Some networks offer either options whilst other networks require you do both.

This has led to quite an amount of friction in the payment process with some clients not receiving the one-time password via SMS whilst others wait and wait and never get the MTN prompt to complete their transactions.

Whilst we certainly do hope that MTN is able to bring down the level of fraudulent transactions on their network, we also hope they’ll encourage easy online payments in Ghana by making the process simple again.

With all that said, we have a gallery below of the various checkout processes of the payment providers. We sadly couldn’t get current screenshots for Hubtel, Interpay and myghpay. (If you have any of these 3 payment providers integrated on your site, do let us know.)

You can click/tap on an image below to see the larger version and follow through the checkout process for that provider.

Reviews and Ratings

As we’ve mentioned earlier, we’ve used about a dozen payment processors over the last decade and we’ve seen almost every type of issue you can imagine.

Issues like chargebacks, systems down, massive hacks, corrupted data and missing information, account shutdowns seemingly fraudulent actions and even cat-and-mouse games to avoid paying out money received. (We should probably write a book!)

In studying the reviews of the various payment platforms, we weren’t surprised to come across customer support issues again, just as we did when we studied the reviews of ecommerce websites in Ghana.

Interestingly, my personal opinion is that poor support might be a thing with the IT industry specifically. Because IT has to do with efficiency, the less human contact required seems to be proof that the system is efficient.

Due to this fact, they end up not talking to customers at all, and that can be frustrating.

Considering the emotions attached to people’s money, not responding swiftly to client issues and complaints makes for very bad business.

When you encounter issues, as you most likely will, it is important that you are able to contact someone who can have your problem solved quickly and pleasantly!

All the payment processors provide email addresses and phone lines via which they can be contacted. Some also provide support over social media channels like Facebook and Twitter. Others provide a live chat option inside your account.

The quality of support is a bit subjective to measure though for a few reasons. A payment processor may provide great support via social media or some other channel but that might not be your preferred communication channel.

Alternatively, a processor might have great support but somehow, you keep getting in contact with the one person that’s not-so-great.

Apart from just support issues, let’s see how the payment processors fared based on their Facebook reviews and ratings.

All 10 payment platforms have (or had) a Facebook page. Interpay and theteller’s pages are no longer active.

expressPay, iPay and myghpay do have pages on Facebook, but they’ve disabled the review sections. Because of this, we aren’t able to tell whether they have received good, bad or any reviews at all over the life of their service.

For the remaining 5 who have their reviews publicly displayed, DPO came out on top with a 4.6-star rating. Slydepay was second with 4.1 and Paystack was third with 3.9.

We do recommend reading through the reviews of any payment processor you plan on signing up with. We’ve highlighted a few reviews earlier by concerned customers but you’ll also come across some great ones.

Disclaimer: If we were moved solely by bad reviews, we would not have a single payment processor to work with.

That’s because no payment gateway is perfect. They all encounter issues here and there, or a few customers get caught up in a perfect storm, leading to them having a horrendous experience.

Settlement

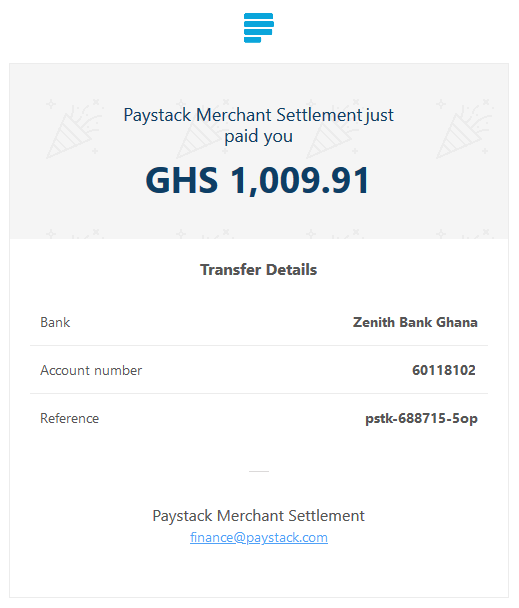

Settlement simply refers to how quickly you’re going to get your money from the sales you make. No one likes to be parted from their money for long.

Usually when signing up for a payment processor, they let you provide details on where you want your money paid to. This is usually to a bank account but can also be to a mobile money wallet in some instances.

Every online payment solution requires time for the payments you’ve received to actually be transferred to your bank account. That’s because of how money moves in our financial system.

Card payments for example are usually settled within 2 to 3 business days. Keep that in mind so you aren’t surprised when payments you are expecting don’t land in your account over the weekend or on a holiday.

In Ghana, mobile money payments are much simpler and so they can usually reflect in your bank account within 24 hours.

You will most likely receive an email and/or SMS notification whenever there’s a settlement by your payment processor.

If your clients pay you mostly via mobile money, then your payment processor will likely have that money in your account within 1 business day. If payments are via cards, then you can expect a delay of about 2 to 3 days.

International card payment settlements can take even longer. You may have to wait 5 business days before they show up in your bank account.

As with almost everything in the world, something that works great for one person might not work so great for another.

Whilst payment providers state how long it takes for money to reach your bank account, not all of them always abide by those timelines.

Popularity

Gauging the popularity of the payment gateways presented a few challenges.

Whilst each of them will allow you to accept payments on your website, they also have other features and differences.

For example, some of the payment processors are popular because they provide terrific offline or point-of-sale (POS) systems, like Hubtel.

Others are popular because they have mobile apps that allow users to send money and make payments for an array of utilities, bills and more, like expressPay and SlydePay.

Jumia, which is now getting deeper into the online payments space, is doing so on the back of the popularity of their own payment system, JumiaPay. It processes payments on the largest ecommerce website in Africa.

Similarly, one of Hubtel’s recent aims has been to house as many stores and online merchants as they can on their own online shopping mall where the payments are processed exclusively by them.

But we wanted to know which payment provider is the most popular for people who have their own websites and want to integrate a payment solution into them.

So we turned to the most popular website platform in the world, WordPress.

We decided to look at how popular a payment processor is by the number of active installations of their WordPress WooCommerce plugin.

The WordPress plugin repository houses over 50,000 plugins of which all are free. They also give an idea regarding the number of active installations of a plugin.

Whilst Slydepay and Interpay both have WordPress plugins, these haven’t been submitted to the repository.

They rather you download these plugins from them directly. Because of that, we can’t tell how popular those plugins are by this metric.

Paystack was far and away the most popular of the plugins installed with over 10,000+ active installations.

Recently, WooCommerce entered into an official partnership with Paystack, making them their preferred payment partner for Africa.

Flutterwave was in second position with a combination of two plugins getting them to 4,000+. DPO was third with 400+ active installations.

Hubtel, expressPay, iPay and myghpay were all tied for fourth place with 200+ active installations and finally came theteller with 90+ active installations.

The top 3 are all companies that provide their payment services in multiple countries. If the most popular payment processor in Nigeria or another part of Africa also launches in Ghana, we believe that is something to consider.

PayPal is probably the largest payment gateway in the world. We were promised that they were arriving in Ghana in 2020, but that has since elapsed.

Whilst that dream is beginning to look a little distant, Ghanaians interested in accepting payments online would still be excited when they arrive.

Account Management

Once you’ve settled on a payment gateway you like (or maybe two) and have integrated them into your website, you’re now going to have to manage your customers, payments, invoices, chargebacks, notifications and so on.

You’d do this from an online console. Depending on the login link and details provided, you’d usually enter your email address and password in order to log in.

A few payment providers offer more than one way to access and manage your account.

Paystack for example provides Paystack Go, a mobile optimized account management area along with a mobile app, Paystack Merchant on both Android and Apple devices.

Once logged into your management console, there should be an array of things you can do.

These include managing your transactions, viewing customer details, handling disputes and chargebacks, managing payment links and even products, sending out invoices and many other settings.

A lot of processors provide graphs of payments you’ve received and even analytics of who is paying, when they’re paying, what methods they are paying via and a lot more.

Backup payment gateways

No matter how great your payment processor is, we have found it incredibly useful to always have at least one backup payment gateway.

In case a transaction doesn’t go through on one, you’d at least be able to send your client through the other gateway and hopefully record a successful transaction.

One of the reasons to have a backup option is because there can be seasons of success or failure. A payment provider might be doing really, really excellent work, but then it suddenly drops off to unacceptable levels.

Perhaps they wanted to gain market share and once they did, they got a little cocky. Or a series of decisions behind the scenes have led to a drop in quality, affecting your transactions.

Or they might still be excellent, just that for some odd reason, your account seems to be encountering issues constantly.

We have had payment processors we recommended far and wide and were satisfied with ourselves, only to have their service become inexplicably unusable and unreliable within a short period of time.

To save you stress, heartache and lost sales, we recommend you have a main payment processor, and at least one backup. (We live by this rule and have multiple payment gateways on standby.)

Get your free website audit instantly!

Conclusion

That pretty much covers the 10 best payment gateways in Ghana and why we believe you should consider them if you want to accept online payments. Certainly if something changes, we’ll have this list updated for you.

Until then, if you’ve got a question or clarification, we’d love to hear from you or you can leave us a comment below.

Thank you for this educative and informative piece. It was a timely discovery.

Keep the good works up!

It was our pleasure, Bennett. Thanks for reading.

Excellent Job guys. Really appreciate your meticulous research presentation. I think we should move the discussion a step further to encourage these platforms to look at how to be competitive on the charges seeing that your reviews are getting global views and also informing customers on which platform to go for. Congrats

It’s our pleasure, Vincent. Thank you.

You make a good point. The platforms being more competitive on their charges and services would be very useful. But it seems the market may have a problem. The number of businesses or merchants who sell their items through a payment processor on their website has to be an encouraging number for the payment processors to keep on investing.

What we’ve noticed is that outside of some of the much larger ecommerce players, the rest of the ecommerce game is played via cash on delivery, and direct mobile money payments. Customers are currently much more comfortable with those than anything else.

Great article. It is rare to come across such a detailed explanation. Thank you.

You’re most welcome, Ralph. It’s our pleasure.

@WopeDigital i read this a while back in 2020, great info but please is this up to date? In terms of rates.

Hi Tim, thanks for commenting.

For service providers whose rates are publicly available, the article is up to date. But a vast majority are quite secretive when it comes to their rates. We do update this article whenever we have new information however we recommend contacting the payment providers directly for the most accurate rates they offer.